I $WISH...

Why I think the shopping app is undervalued.

Wish—the shopping app—has been having a rough 2021 (honestly, who isn’t!?). The stock is down ~80% since its IPO last year. Naturally, I thought now would be the perfect time to load up on some shares. A few reasons why…

Wish is Undervalued

Value/discovery shopping is a misunderstood retail experience. Most investors don’t like to shop this way but LOTS of consumers do

Yes, Wish saw a 13% reduction in app installs and 32% reduction in marketplace revenue in Q2 but was still the #4 most downloaded shopping app globally in H1 2021, has 90M MAUs, and average order value (AOV) has been trending upward the past few quarters.

The current valuation basically equals Wish’s cash on hand ($1.6B) + annual revenue run-rate ($2.6B). Going below this would indicate investors have no confidence in the management team to turn things around.

Speaking of the management team, Wish recently overhauled their entire executive suite: added Jackie Reses (of Square fame) to their board as Executive Chair (May 2021), hired CTO (July 2021), fired CFO (July 2021), hired Chief Product Officer (Aug 2021), fired VP Operations (August 2021). This could be cause for concern, but I’m looking at the changes optimistically.

Despite all of this movement (on the exec team and in the stock price) I see a company that has already started laying the foundation for a nice growth flywheel based on e-commerce logistics.

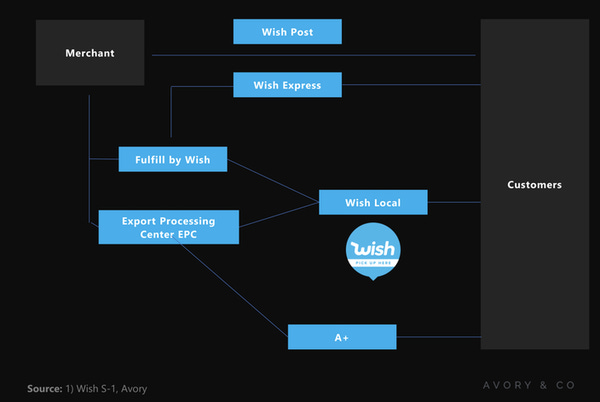

Wish Logistics

Logistics as a Platform:

Wish can offer their logistics to merchants selling on their marketplace or as a third-party provider for merchants selling elsewhere. As a third-party logistics vendor, they can more easily entice the merchants to list products on Wish as well, increasing assortment, availability, and time to door (TDD). Wish’s CEO, Peter Szulczewski, explains more here.

Wish Local:

Last-mile logistics are hard and this is where Wish is building out its biggest moat and long-term value driver.

They have 50K merchants on Wish Local, which are merchant locations that receive customer deliveries—acting as a distributed fulfillment center with no CAPEX for Wish.

Consumers benefit by getting lower costs and access to faster shipping times by selecting a local “pick-up” center as their delivery option.

This option is gaining traction: 25% of orders in markets such as Mexico and Italy are done through Wish Local.

Other Logistics:

90% of orders are shipped through some version of Wish’s logistics platform.

Wish’s logistics system helps standardize the merchant experience, driving down TDD and often allowing Wish to verify products before they’re shipped to customers. Shipping times and product veracity/quality are the biggest customer complaints.

Fulfillment by Wish allows merchants to forward-deploy inventory (usually from China to local markets), which increases availability and decreases shipping time.

Wish's Flywheel

Wish can use its logistics platform to increase # merchants, inventory, availability, and assortment on the platform. Which will attract more customers.

Attract and retain value-conscious consumers with a robust assortment of low-cost goods, decreasing time-to-door (TTD), and high availability.

Use increasing customer base and last-mile logistics platform to attract merchants in higher AOV categories such as grocery and consumer packaged goods.

Bonus: Retain users via financial services such as merchant or consumer financing, stored value based on purchase behaviors to incentivize loyalty (Wish Cash), etc.

Takeaways & Acknowledgments

Takeaway:

Apple’s recent iOS 14.5 changes seriously undermined Wish’s user acquisition strategy, which was based primarily on digital advertising. I believe this setback will lead to a more diversified user acquisition/retention strategy in the long run and Wish has already started laying the foundation for a nice flywheel based on e-commerce logistics.

Acknowledgments:

Thanks to Avory Research for this amazing analysis of Wish and to Turner Novak for the general bullishness on the company, which got me to take a look.