Adyen: Payments & Profitability

Why I’m Bullish on Payment Companies, Adyen’s Payments Profitability Playbook, Stripe’s New Refund Policy, & Checkout.com’s Crypto Conundrum

Many public company stock prices have come down dramatically over the last 12-18 months, so it’s no surprise that private payment company valuations have come down as well. Among the major payments companies I track*, this is how far each stock price / valuation is off its all-time high:

____________________________

|Company |Δ from ATH |

|Fiserv | -17.9% |

|Stripe | -34% |

|Global Payments | -49% |

|Adyen | -50% |

|FIS | -54% |

|PayPal | -74% |

|Checkout.com | -74% |

––––––––––––––––––––––––––––Pretty grim. But there are brighter days ahead for (some) of these companies.

Why I’m Bullish on Payments

I think digital payments is an incredibly resilient category and—if operated in a disciplined way—has one of the most incredible business models ever created:

Payments has one of the largest total addressable markets (TAM) possible. To believe the category of payments will grow, one just has to believe that GDP will continue to grow and become more digital.

Payments are ubiquitous. I understand the complaints about “rent-seeking” but I think charging 20bps + 10¢ in transaction fees for global, secure, and highly-available access to a payments network with hundreds of millions of customers is a pretty fair trade. From a business perspective, charging what is essentially a consumption tax on something that resembles (or exceeds) GDP is a pretty good way to make money.

Payments is also incredibly resilient. If a payments company does a good job providing reliability, security and/or network effect, they encourage new transactions to take place on their platform and revenue compounds.

Payments is a natural inflation hedge. If the price of a gallon of milk increases, the underlying payments providers—charging their consumption tax—will take a proportionally larger amount as gross revenue.

Payments is profitable (at scale). Payments have relatively thin unit margins but their overall profitability is an “area under the curve” equation and, luckily, businesses tend not to switch payment providers very often, giving them a long time to charge their consumption tax.

Payments are agnostic of whether the dollar (or euro, peso, etc) spent is for goods or services or whether the transaction is in-person or online. As we saw over the last few years, consumer spending can switch rapidly between channels. Most modern payments providers (the technologically agile ones) now offer a unified view of payments processing across channels because their customers are demanding it. This will set them up to weather any future storms like the covid-19 pandemic.

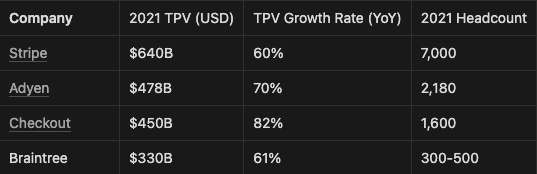

Most companies in the table above will rebound to some degree but I’m especially bullish on the modern payments providers: Adyen, Stripe, Checkout, and (to a lesser degree) Braintree, a division of PayPal. These are companies growing total payments volume (TPV)—and therefore gross revenue—at 60-80% y/y from a base of processing hundreds of billions of dollars.

I don’t know the specifics of how each business is run since two are still private and PayPal only hints at Braintree’s performance, but each has a clear playbook to follow to improve their net revenue margins.

Adyen’s Payments Profitability Playbook

Adyen wrote the payments profitability playbook. The business has been throwing off cash for years, achieving ~60% EBITDA margins, and is more profitable, on a per-employee basis, than Netflix, Apple, Google, or Facebook. They’ve done this while maintaining impressive growth rates (40-60%) and shipping new products at a decent clip. The keys to their success have been:

Close large customers (TPV)

Expand payments volume (gross revenue)

They do this by gaining a larger proportion of that merchant’s payments volume and/or retaining that customer as they grow.

80% of new revenue in any given period comes from existing customers. That’s some nice net dollar retention.

Accept that their take rate will decline over time (net revenue)

From their H2 2021 shareholder letter: “The gradual decline in take rate…is a natural consequence of our business model and the execution of our strategy of onboarding profitable volume at scale—which has always predominantly come from enterprise merchants.”

Remain disciplined, mainly by limiting headcount (opex)

Part of remaining disciplined for Adyen has meant being late to certain categories due to their relatively focused R&D. For example, they didn’t add platform payments, card issuing, or Banking-as-a-Service capabilities until they were at risk of losing volume from existing customers (see #2) or losing out on a meaningful number of new deals (see #1). Instead, Adyen waits to see if there is a business need (not just a general market trend) for new services, then goes all in if there is.

That focus allows them to move quickly once they’re committed to a product area (e.g., adding new payment methods/modalities). This is how Adyen, which I just characterized as disciplined and cautious, was the first non-Block payments provider to offer Cash App Pay, and (hilariously) beat Stripe to offering Apple’s Tap to Pay capability despite Stripe and Apple going out with a press release saying Stripe would be the first provider to offer it. Acquiring relatively larger customers, expanding revenue from existing customers, and focused R&D means Adyen can run a business with TPV comparable to Stripe’s with 1/3 the headcount, which leads to those high 50s / low 60s EBITDA margins.

New Years Resolutions for Payment Companies

As macro conditions worsen, I expect IPO-bound payments companies like Stripe and Checkout to emulate Adyen’s discipline as profitability becomes something of a New Year’s Resolution for each company. Here’s what they’ve been up to lately:

Stripe and Checkout both lowered their own internal valuations to attract/retain talent but it has the added benefit of decreasing the cost of their stock-based compensation (SBC). Adyen’s SBC is relatively low, in part, due to a Dutch regulation that prohibits financial institutions from offering more than 20% of an employee’s compensation as “variable remuneration.”

But there are other cultural differences between how the companies operate. Gergely Orosz has some of the best commentary on the Stripe vs. Adyen engineering compensation philosophies specifically:

Last November, Adyen published a letter entitled: “Growing our team in a disciplined way as we build the future of Adyen,” just weeks after Stripe announced it was laying off 14% of its staff. Checkout announced a 5% layoff in September. You can imagine both layoffs are intended to get operating costs more in line with a public comp like Adyen and are necessary if the companies are pulling back on their frontier R&D investments. Going forward, expect Stripe and Checkout to start managing their operating expenses more tightly.

Stripe’s New Refund Policy

Stripe recently introduced a change regarding how they’ll handle refund fees for businesses on interchange+ pricing going forward (learn more about interchange here):

Changes to refund fees

Variable fees for transactions that get refunded: Stripe charges a variable fee for all transactions, and returns this fee for all transactions that get refunded. From March 1, 2023, we will no longer return this fee.

Fixed fee for refunds: Stripe charges a fixed fee to your account each time we interact with the card networks on your behalf. This fee is specified in your contract and is intended to cover our costs. A refund, like all other transactions, requires interaction with the card networks through Stripe. Starting March 1, 2023, we will begin charging this fee for all refunds.

So not only will they begin keeping the variable fee they used to return to a merchant in the event of a refund but they will also start charging an additional fixed fee each time they initiate a refund for a merchant.

Stripe’s refund policy has evolved a lot over the last decade. In 2012, they proudly touted “no fees on refunded charges” in a pricing update but somewhere between then and now they stopped returning processing fees for refunded transactions and began charging fees for some refunds. The timeline I’ve been able to put together is:

2012: No refund fee and processing fees returned (source)

2017: Processing fees not returned but no refund fee for new merchants (source)

2020: Processing fees not returned but no refund fee for all merchants (source, source)

2022: Processing fees not returned and a fee for qualifying refunds for all merchants (source)

I can’t be 100% sure why Stripe felt the need to expand this policy further but it’s in line with their publicly traded peers—namely Adyen and PayPal—and is a clear example of Stripe getting their operating costs in control.

Checkout.com’s Crypto Conundrum

Checkout.com recently released a “Full Account” of their UK-based operations. It gives some insight into other European operations as well but it’s only a partial view of a company that has operations across the Middle East, Asia, and North America as well. That said, one can piece together some idea of the company’s 2021 performance. Investor and Batch Processing Pal, Gonçalo Fernandes, did just that. He points out that Checkout grew UK-only revenue 82% YoY and estimates $350M of net revenue with $280M of operating expenses, a 20% margin. That’s not bad but well under the 63% EBITDA margin Adyen reported for 2021.

And no, crypto doesn’t solve this. According to reporting from the Financial Times, nearly 50% of Checkout’s payments volume in 2021 came from fintech and crypto clients when “Binance was the company’s top merchant by net revenue.” I am NOT knocking Checkout for courting crypto companies and supporting crypto transactions. I’ve built my career building payments companies that support relatively new types of merchants. Checkout also deserves a lot of credit for identifying a category experiencing enormous growth that had few providers serving it. That’s a smart way to grow payments volume.

What I don’t understand is how Checkout has such low operating margins. Credit Suisse estimates Checkout and Adyen’s TPV were similar in 2021 ($450B vs. $478B) and Checkout had about 3/4ths the number of employees (1.6K vs. ~2.2K) in 2021. Assuming they have similar per transaction take rates, Checkout should have similar operating margins as Adyen. But they don’t.

If anything Checkout’s take rate should be higher than Adyen’s:

Checkout serves relatively smaller customers than Adyen, which is known for its enterprise-scale clientele. Larger customers can demand lower rates.

Crypto was a booming category for most of 2021, which could explain the eye-popping 82% revenue growth in the UK, but crypto was/is also relatively underserved and volatile. Checkout can and should be able to charge a higher fee relative to Adyen for jumping through all the regulatory hoops and taking on the financial liability for a such high-risk category like crypto. There is a similar dynamic when processing payments for adult content or cannabis products where 5-8% processing fees aren’t unheard of.

We will have to wait until Checkout goes public to get a better sense of their full financial health but I worry about their near-term prospects as crypto volume continues to fall. In the meantime, they seem focused on growing volume in new regions and with new products like card issuing (coming in 2023).

* Disclosure: I own shares of Adyen, PayPal, and Stripe*

Cutoff Time

Cutoff Time is a section of Batch Processing that includes interesting links to news or ideas that caught my eye but decided not to write about in this batch:

Affirm now finances ~2% of US e-commerce spend, per Octahedron Capital.

Gas stations are a difficult payments merchant category to underwrite due to high fraud and metrics certification, per Fintech Dion.

Visa Direct’s payment volume is larger than I expected: ~600B in 2022, per Sid Singh.

Mastercard has doubled the size of its acceptance network in the last 5 years! per Matt Cochrane.

Visa & Mastercard are not in danger of a credit/lending pullback per East Cap.

This batch was powered by: